Every business wants to be more innovative. Yet almost every business struggles to make innovation work. In this article we take a pragmatic look at how too make innovation more successful for your organization and offer alternatives to help you find better avenues to exceptional growth.

The uncomfortable truth: most business models have expiry dates.

What's worse is that large businesses are almost immune to being changed from the inside.

No amount of migrating to the cloud, agile methodologies, or investing in AI will change this.

Table of Contents

- Every business wants to be an innovator

- Big vs Innovative

- What about innovation teams?

- The three types of innovation

- Making innovation work for your business

Virtually every business wants to be an innovator

Innovation comes naturally to startups and scale-ups of course, they're in business to disrupt industries and steal share from large incumbents.

But what if you ARE one of those large incumbents?

Many CEOs lose sleep over new entrants coming for their lunch. They worry about their ability to evolve fast enough to survive and thrive in an increasingly VUCA (volatile, uncertain, complex, ambiguous) world.

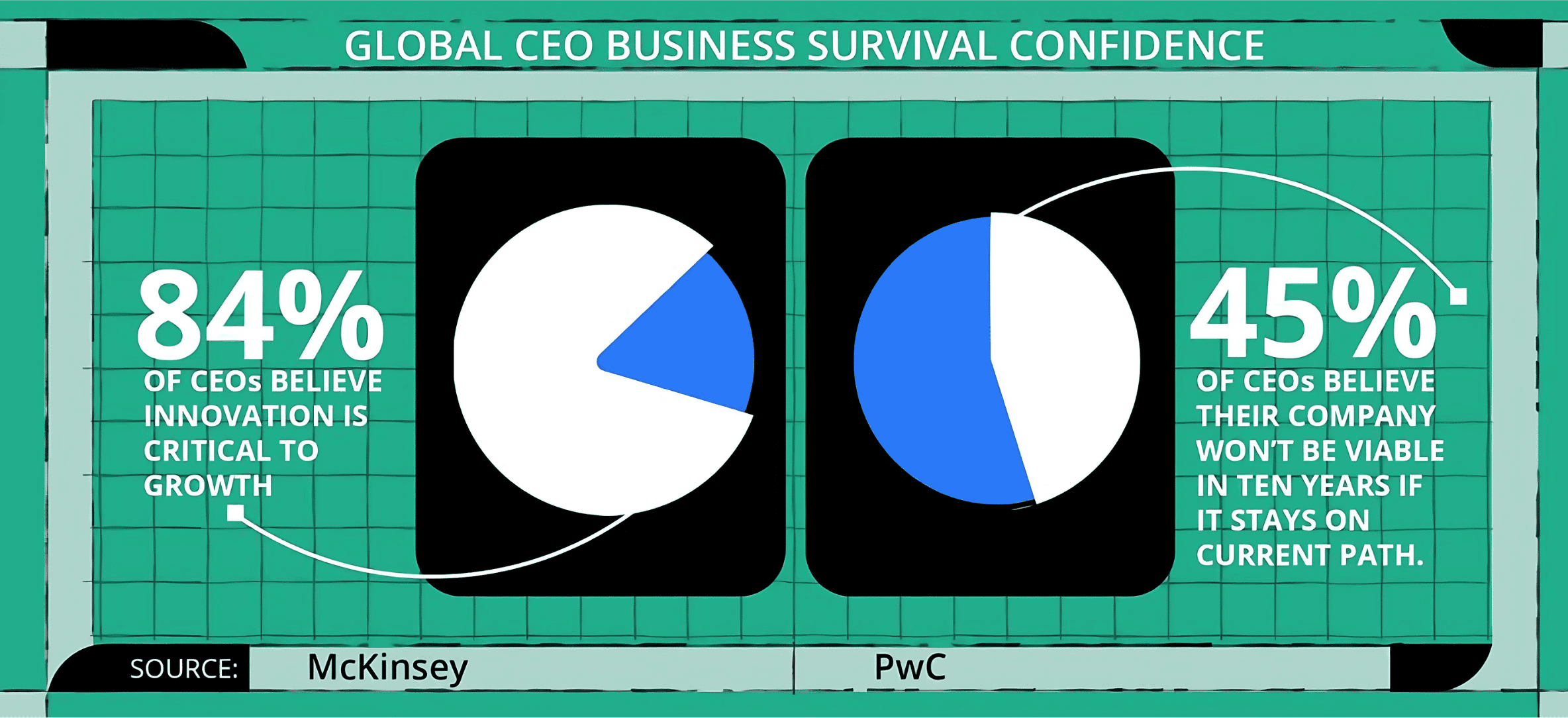

So it’s not surprising we see data from PwC finding that 45% of CEOs believe their company will not be viable in ten years if it stays on its current path.

The drivers for change are many and varied (and becoming more urgent).

Changes in technology (hello AI), shifts in how and what people buy, government regulations, competitor activity, climate change—it’s the perfect storm for an end to business as usual.

Yet the data also shows that just 6% of CEOs are satisfied with their innovation performance.

And digital transformation? On average, 87.5% of digital transformation initiatives do not meet their original objectives.

As businesses, we know we need to innovate but all the indications suggest we’re failing.

Big vs. Innovative

Large established businesses rarely get to their size and scale overnight. They build their capabilities year after year, growing their products and expanding their markets.

Maturity sets in. And with it comes more complex governance, slower decision-making, and greater risk aversion. Existing cash cows must be protected. Current customers must get what they expect. Big scary changes are only considered when things are going terribly wrong.

Change in a large complex organization is difficult (and difficult to agree on). What makes sense in theory often faces so many implementation issues that it never sees the light of day. And promises of magical fixes such as “digital transformation” evaporate when they meet the realities of the existing business.

This is at the core of the Innovator’s Dilemma. As its author Clayton Christensen demonstrates, even successful, well-established companies can fail when faced with disruptive innovations despite doing everything "right" in theory.

The dilemma stems from the fact that these companies have powerful incentives countering their innovative good intentions. It leads them to focus on existing customers and products. Change becomes painfully slow and, at best, iterative.

This makes them more vulnerable to new, disruptive technologies and business models.

What about innovation teams?

The solution for many large businesses is to create separate teams tasked with developing new products and thinking new thoughts. They are often somewhat insulated from the core business, given freedom to explore new products and business models.

So how do they perform? The picture is mixed:

- The Bosch Accelerator Program invested in 200 teams over three years. This led to 15 projects being taken to scale with follow-on funding (7.5% success rate)

- The Sony Startup Accelerator Program (SSAP) has so far developed over 750 business ideas and created 14 businesses (1.9% success rate)

- On a smaller scale, steam iron maker Laurastar’s innovators developed 14 ideas and one was successfully executed (7% success rate)

These are hardly the kinds of returns likely to meet CEO and shareholder ambitions.

However, to be fair, this is simply a reflection of the hit rate of many innovation programs. The reality is, the failures will always massively outweigh the successes. Every. Single. Time.

The challenge is to spot each early so that you can either kill off a poor performer quickly or invest in a potential winner for the longer term.

The three types of innovation

Part of the problem of innovation is even agreeing on what we mean. It’s a term that gets thrown around by businesses of all types (not to mention gurus eager to sell their latest book).

It sounds good. Who doesn’t want to be innovative?

We could look at one of the standard definitions such as the OECD’s version: innovation, they say, is “the implementation of a new or significantly improved product (good or service) or process, a new marketing method, or a new organizational method in business practices, workplace organization or external relations.”

But does this get us to anything practical?

For the purposes of this article, we’ll split out innovation by its proximity to the core business. This gives us three main strategies:

- Sustaining innovation

- Detached innovation

- Adjacent innovation

Each demands a different approach. And each will deliver very different results. We’ll present an overview below.

It's time to get Unstuck

If you're leading an established business with persistent growth challenges, we've published a new in-depth framework which includes a detailed look at our Growth Sphere Model.

In the framework, we explore why so many large organizations struggle with growth. Finally, we unpack the most-used strategies deployed by businesses today. We analyze their pros and cons and highlight why you may or may not want to explore them for your business.

It's time to get Unstuck

If you're leading an established business with persistent growth challenges, we've published a new in-depth framework which includes a detailed look at our Growth Sphere Model.

In the framework, we explore why so many large organizations struggle with growth. Finally, we unpack the most-used strategies deployed by businesses today. We analyze their pros and cons and highlight why you may or may not want to explore them for your business.

1. Sustaining innovation: evolving the core

Sustaining innovation centers around delivering improved performance across existing products. It’s about upgrades and new versions—the latest smartphone, a new colorway of sports shoe etc.

This kind of innovation builds on the business’s current processes and cost structures. Companies tend to use in-house teams who’ll iterate new offerings based on customer feedback and market demand.

The results will sit firmly in the core organization however. We won’t see a new business emerge as a result.

The good news here is that these innovations will be built around in-depth product and customer knowledge. As such, this is relatively low risk. It’s more of the same but better (and potentially cheaper or more profitable depending on business focus).

The not-so-good news is that these approaches rarely produce anything ground-breaking. It’s the Innovator’s Dilemma writ large. You can get this right and still fall victim to a fast-moving competitor who takes a very different approach.

2. Detached innovation: blue skies thinking

At the other end of the proximity spectrum is the detached (or non-adjacent) approach. This is the classic territory of the dream-big, blue-skies innovation team. Nothing is off-limits.

At this level, proposed innovations need have very little to do with the core business. The result will typically be a new standalone business selling new products and services to new customers.

But as Clayton Christensen points out, of the nearly 30,000 new products introduced each year, 95% fail. Other statistics indicate around a 90% failure rate for new startups.

The odds are not stacked in your favor.

While detached innovation offers the promise of a wide-open playing field, it has a significant drawback.

It typically ignores what the business already knows about its markets and customers. The whole idea is to break free in a completely new direction. But this demands the new entity invests in customer research, talented people, and new capabilities. This will cost significant time and money.

It is very high risk.

3. Adjacent innovation: the Goldilocks option

In the middle we find adjacent innovation. This focuses on creating new product offerings and business models that are in the same orbit as the organization’s core.

Unlike sustaining innovation, adjacent approaches do represent a significant shift away from an organization’s traditional business.

While the resulting products and services will be able to leverage the capabilities and assets of the core business, they will be an entirely new offering in the market.

This is key. Close but not too close.

New ventures should be able to be kept separate from the legacy business (but not so separate that they can’t benefit from the parent’s protection and support)

As with all innovation, failure rates will still be significant. Those who succeed will spread their bets, especially in the early phases. The trick is to be ruthless about what’s allowed to continue (and receive additional investment) and what gets killed off.

This demands high-quality data and in-depth experience.

Making innovation work for your business

No innovation is risk-free. Risk is the nature of the beast.

Making it work demands finding the sweet spot between overly cautious iteration (as seen with too many sustaining innovation programs) and reckless abandon (detached innovation, we’re looking at you).

In our experience, for most businesses most of the time, adjacent innovation offers the greatest results for the investment involved.

Want to discuss how Stryber can help?

Finding growth from your core: when to pursue market penetration strategies

The 8 great myths of corporate innovation